shares Palantir Technologies (NYSE: BLT) It fell 8% despite the company reporting strong first-quarter results and increasing its full-year guidance.

Let’s take a look at the company’s quarterly results, why the stock is falling, and whether this is a buying opportunity for long-term investors.

Re-accelerate growth

Palantir reported strong first-quarter results, with revenue growing 21% to $634 million. This represents the third consecutive quarter of accelerating revenue growth. Its revenue growth reached its lowest level at 13% in the second quarter of 2023, before accelerating to 17% in the third quarter and 20% in the fourth quarter of last year.

Commercial revenues jumped 27% to $299 million, driven by a 40% increase in U.S. commercial revenues to $150 million. Excluding strategic commercial contracts, commercial revenues rose 36%, with U.S. commercial revenues increasing 68%, it said.

The company added 41 new customers to its US business, while also saying it was seeing strong expansion among existing customers. Palantir credited its artificial intelligence platform (AIP) for strong commercial growth in the US, as well as its continued focus on “Bootcamps,” which it uses to introduce AIP to new customers. She used the example of a large utility company signing a seven-figure deal just days after completing boot camp.

Meanwhile, international business revenues grew 16% to $149 million, but fell 3% sequentially. The company said it continues to see headwinds in Europe and that there was a revenue increase in the fourth quarter that it did not see in the first quarter.

AIP offers the largest potential driver of future growth for Palantir, so its rapid adoption among U.S. commercial customers is a big positive. The company has shown that not only does it have a strong product, but its go-to-market strategy through its bootcamps is also working. However, the relatively modest growth out of Europe, which represents about 16% of its business, is a bit disappointing. Palantir discussed the weak macro backdrop in Europe, however Artificial intelligence platform It should be able to help reduce costs, and this type of business should not be affected by overall weakness.

On the government side of the business, revenue rose 16% to $335 million. U.S. government revenues were up 12% year-over-year, and rose 8% sequentially to $257 million. Palantir noted that it is the sole contractor in the Army’s TITAN (Tactical Intelligence Targeting Node) program and that it expects to see further growth in its US government business throughout the year. Intergovernmental revenues rose 33% year over year, but fell 9% sequentially to $79 million.

Palantir’s US government business is improving, but overall growth remains relatively modest. This can be a lumpy business; However, given the current geopolitical tensions, it is a bit disappointing that the business is not growing more quickly.

Palantir raised its full-year revenue forecast to a range of $2.677 billion to $2.689 billion, above its previous revenue forecast of $2.652 billion to $2.668 billion, and also revised its revised operating income forecast to a range of $868 million to $880 million. From $834 million to $850 million.

For the second quarter, it expects revenue to be between $649 million and $653 million, and adjusted income from operations to be between $209 million and $213 million.

Why did the stock fall?

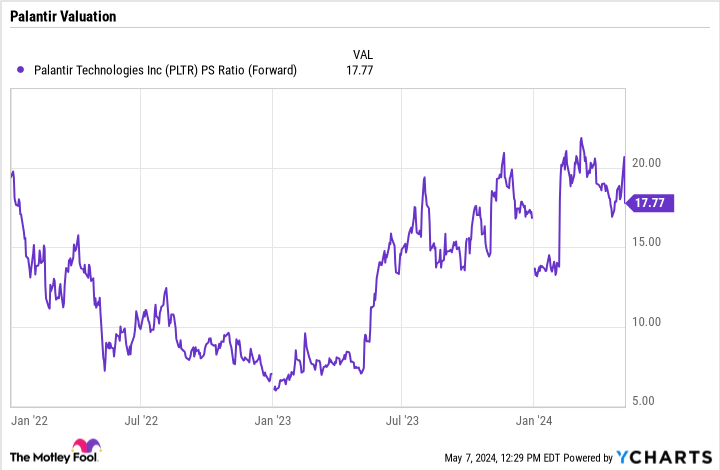

One of the main reasons Palantir stock is sinking despite its strong results is the stock evaluation. The stock currently trades at roughly 18 times forward sales, a high multiple for a company whose revenues are only growing in the 20% range, and which outpaced earnings by more than 20 times before the stock sold off. To justify this valuation, the company needed to see signs of growth accelerating more than they already are.

While Palantir increased its full-year revenue guidance, the high end of its full-year forecast still represents just 21% growth compared to 2023 when it posted revenue of $2.225 billion and analysts have generally been looking for the company to raise its guidance higher. The company beat the high end of its first-quarter revenue guidance by about $18 million, but only raised the high end of its full-year guidance by about $21 million. Much of the increase in guidance comes solely from increased first-quarter revenue, without much follow-through expected.

Meanwhile, sequential declines in European commercial and international revenue growth are also somewhat worrying in light of the stock’s valuation. Although its US government business is improving, it is still the slowest-growing segment.

Is it time to buy the stock?

Palantir stock has seen a significant rise over the past year, and much of that has been due to the expectation of much higher future revenue growth driven by AIP. While AIP has a lot of potential, it hasn’t added enough to overall revenue growth at this point to justify Palantir’s valuation.

Even with the recent sell-off, Palantir’s valuation has not fallen enough to justify trading at 18 times forward sales. I would need to see the stock price decline or have signs that growth will return to more than 30% before I buy the stock.

Should you invest $1,000 in Palantir Technologies now?

Before you buy shares in Palantir Technologies, consider the following:

the Motley Fool stock advisor The analyst team has just defined what they think it is Top 10 stocks Let investors buy it now… and Palantir Technologies wasn’t one of them. The 10 stocks that were discounted could deliver huge returns in the coming years.

Think when Nvidia I prepared this list on April 15, 2005… If you invested $1,000 at the time of our recommendation, You will have $550,688!*

Stock advisor It provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. the Stock advisor The service has More than four times The return of the S&P 500 since 2002*.

*Stock Advisor returns as of May 6, 2024

Jeffrey Seller He has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Palantir Technologies. The Motley Fool has Disclosure policy.

Palantir increased its guidance, but investors are selling. Is it time to buy stocks? Originally published by The Motley Fool

“Explorer. Unapologetic entrepreneur. Alcohol fanatic. Certified writer. Wannabe tv evangelist. Twitter fanatic. Student. Web scholar. Travel buff.”